Israel

country profile

April 2026

Israel remains a global leader in outbound travel, with a remarkably resilient market. In 2025, Israeli outbound travel achieved a historic milestone, reaching approximately 9.42 million trips—surpassing pre-pandemic peaks and demonstrating a full recovery from the downturn in early 2024. While Europe and the Eastern Mediterranean remain traditional favorites, 2025 and 2026 have seen a significant pivot toward safe, nearby, and culturally welcoming destinations.

Geographical proximity continues to dictate travel habits, with over 90% of trips made by air. While Greece, the US, and Cyprus remained top-tier flight destinations throughout 2025, the market saw explosive growth in "safe-haven" and value-driven destinations. Countries like Cyprus (+41% in hotel stays) and the Czech Republic continue to trend upward, while Azerbaijan has established itself as a primary alternative for Israelis seeking a blend of luxury, safety, and authentic heritage.

The aviation landscape has also stabilized; after the 2024 surge where Israeli carriers (El Al, Israir, Arkia) handled nearly 66% of TLV traffic, 2025 saw a gradual return of international giants like WizzAir, Fly Dubai, and United Airlines, restoring competitive pricing and capacity to the market.

The ATB continues to prioritize Azerbaijan’s unique competitive advantages: its rich culture, diverse natural landscapes, and deep-rooted Jewish heritage.

The "discovery phase" that began in 2024 has matured into a sustained demand. In 2025, approximately 70,000 Israeli tourists visited Azerbaijan, representing a massive 139% surge compared to the previous years. This growth was driven by a strategic shift in Israeli traveler behavior; seeking safe, emotional wellness and "soft travel" options, Israelis have moved beyond Baku to discover regions like Guba (Red Village), Gabala, and Naftalan.

Nowadays, the interest is no longer just exploratory, it is structural. Israeli tour operators are now establishing long-term partnerships with Azerbaijani DMCs to handle high-volume groups. Azerbaijan is now viewed by the Israeli market not just as a "new destination," but as a primary, safe, and premium choice for family, business, and heritage travel.

|

Holiday / Period |

2026 Dates |

Description & Travel Impact |

|

Passover (Pesach) |

April 1 -April 8 |

A major 8-day holiday. High demand for family travel. Planning typically begins in January/February. |

|

Independence Day |

April 22 |

Often combined with the surrounding days for short "spring breaks." |

|

Shavuot |

May 21 - May 22 |

A two-day holiday. Popular for short regional getaways and nature-focused trips. |

|

Summer Period |

July - August |

The primary school holiday season. Families prioritize long-haul or comprehensive regional tours (6–8 days). |

|

Rosh Hashanah |

Sept 11 - Sept 13 |

The Jewish New Year. A three-day weekend (Fri-Sun) triggering high outbound volume. |

|

Yom Kippur |

Sept 20 - Sept 21 |

The holiest day. Note: All flights in/out of Israel cease for 24+ hours. Travel usually occurs just before or after. |

|

Sukkot |

Sept 25 - Oct 2 |

An 8-day festival. Significant for "Roots Tourism" and multi-generational family groups. |

|

Simchat Torah |

Oct 3 - Oct 4 |

Immediately follows Sukkot, marking the end of the "High Holiday" travel season. |

|

Hanukkah |

Dec 4 - Dec 12 |

School winter break. Increased interest in "City Breaks" (Baku) and winter activities (Shahdag/Tufandag). |

The contemporary Israeli traveler is a sophisticated explorer, increasingly trading short city breaks for in-depth regional experiences. Characterized by high purchasing power and a deep-seated need for security, this market is currently driven by a "Soft Travel" trend - a search for emotional wellness, nature, and stress relief.

The market is primarily composed of five distinct pillars:

Large Families: As a deeply familial society, Israelis often travel in multi-generational groups of 4 to 15 people, requiring spacious accommodations and diverse activities.

Young Professionals & Couples: Particularly those from the "Hi-Tech" sector, these travelers seek 3–4 annual trips, often focusing on premium weekend getaways and vibrant city life.

Organized Group Tours: Primarily seniors (aged 50+), these groups of 15–25 travelers prefer all-inclusive packages guided by professional agents.

Religious & Heritage Travelers: This segment focuses on "Roots Tourism," visiting synagogues and the Red Village (Guba). They often travel in large, pre-planned groups organized through specialized agencies.

Business Travelers: Strong bilateral economic ties maintain a consistent flow of corporate travelers who often extend their stay for leisure.

While Baku remains the primary gateway, there is a significant shift toward Guba, Gabala, Shaki, Gusar, Ismayilli and the thermal springs of Naftalan.

Wellness & Nature: Seeking relief from Israel's hot climate and regional stress, travelers prioritize thermal springs, mountain retreats, and greenery.

Jewish Heritage: Deep interest in visiting family ancestral sites and historical Jewish monuments.

Gastronomy & Shopping: There is a high demand for authentic Azerbaijani cuisine and kosher-friendly options. Due to high domestic costs in Israel, travelers actively seek premium shopping opportunities abroad.

Niche Interests: Growing interest in LGBTQIA+ friendly destinations and "Interest Groups" such as hikers, photographers, and medical tourists (specifically for dentistry and spa therapies).

Safety and Security: Prioritize safe and stable destinations.

Comfort and Quality: Favor high-quality accommodations and services.

Value for Money: Seek good value and affordable pricing.

Well Planned Packages: Use conservative ways of travel ordering through travel agents.

Average spending by Israeli tourists abroad fell from around USD 3,000 per trip in 2018 to about USD 2,200 in 2022, then partially recovered to roughly USD 2,600–2,900 in 2023–2025, remaining slightly below pre-pandemic levels despite the strong rebound in outbound travel.

Israeli tourists use a hybrid model of travel planning that combines advanced digital tools with a deeply rooted tradition of working through trusted travel agents. While travelers actively gather inspiration and information from online platforms, social media (especially Hebrew Facebook groups), user-generated reviews, and recommendations from friends and family, many final travel decisions are still mediated by professional agents. This is particularly true for families and older travelers, where it is common to work with the same travel agent for decades or even across generations, based on trust, personal familiarity, and proven reliability.

In terms of planning and decision-making, Israeli tourists are generally flexible and relatively fast in their choices. Short-haul and leisure trips are often planned weeks rather than months in advance, while family vacations, holidays, and long-haul travel follow a medium planning horizon. Security considerations, flight availability, and pricing strongly influence the timing of decisions, making Israelis highly responsive to recommendations provided by both digital platforms and travel agents.

Regarding booking channels, online booking plays a major role, particularly for flights and accommodation, with global platforms such as Booking.com and airline websites widely used. However, unlike many other digitally advanced markets, travel agencies in Israel remain highly relevant. Many travelers prefer agents not only for complex itineraries, group or family travel, religious or holiday trips, and destinations perceived as unfamiliar, but also for routine vacations. Agents are valued for their ability to handle changes, provide Hebrew-language support, secure flexible conditions, and offer personalized advice shaped by long-term knowledge of the client’s preferences.

Alongside global booking tools and price-comparison websites, Israeli tourists also use specialized platforms and locally developed travel technologies, particularly for finding deals or optimizing prices. Nevertheless, these platforms often serve as supporting tools, while the final booking is frequently completed by a trusted agent. Overall, Israeli tourists can be characterized as digitally informed but relationship-driven travelers, combining independent research with a strong reliance on long-standing personal connections within the travel-agency sector.

As of April 2026, air connectivity between Baku (Heydar Aliyev International Airport – GYD) and Tel Aviv (Ben Gurion International Airport – TLV) is supported by a high volume of direct flights, with Azerbaijan Airlines (AZAL) playing a central role on the route. Flight schedules vary by season; however, capacity has increased significantly in response to demand.

Looking ahead, AZAL has announced plans to further expand its operations, with the aim of reaching 21 weekly flights by May 2026, effectively establishing a strong near-daily connection between Baku and Tel Aviv.

Israeli air carriers Israir and Arkia currently operate three weekly flights each, with plans to increase frequencies during the high-demand summer season.

Direct flights between Baku and Tel Aviv have an average flight duration of around 3 hours, making the destination easily accessible for short stays and leisure travel. All flights depart from Heydar Aliyev International Airport in Baku and arrive at Ben Gurion International Airport in Tel Aviv, ensuring efficient point-to-point connectivity between the two capitals.

* provided data doesn’t reflect situations of military instability and tension

International Mediterranean Tourism Market (IMTM)

ATB regularly joins the local trade events, information can be accessed from ATB events

Between 2021 and 2025, Israeli tourist arrivals to Azerbaijan demonstrated a clear recovery trajectory following the COVID-19 disruption, culminating in a sharp surge in 2025 after several years of steady, incremental growth.

In 2021, Azerbaijan received 6,655 Israeli tourists, reflecting the early stage of post-pandemic recovery, when international travel was still constrained by health-related restrictions and limited air connectivity. A strong rebound followed in 2022, when arrivals rose sharply to 23,935, representing a growth of approximately 260% year-on-year. This rapid increase was driven by the easing of travel restrictions, the restoration of direct flights, and renewed outbound demand from the Israeli market.

Growth continued in 2023, with Israeli tourist arrivals reaching 29,093, marking a further 21.6% increase compared to the previous year. This period reflects a consolidation phase, in which Azerbaijan strengthened its position as an accessible and attractive destination for Israeli travelers. In 2024, arrivals remained broadly stable at 28,955, showing a marginal decline of less than 0.5% compared to 2023. This slight stagnation indicates a temporary leveling-off rather than a structural downturn, likely influenced by external factors such as regional military situation.

A decisive acceleration occurred in 2025, when the number of Israeli tourists visiting Azerbaijan surged to 69,124, representing a substantial 139% year-on-year increase compared to 2024. This exceptional growth underscores a renewed expansion phase, supported by strong air connectivity, increased flight frequencies, intensified tour operator activity, and rising awareness of Azerbaijan as a leisure destination in the Israeli market.

Overall, the 2021-2025 period illustrates a transition from post-pandemic recovery to robust market expansion, positioning Israel as one of Azerbaijan’s fastest-growing source markets in recent years.

Source: State Tourism Agency

A significant portion (79.4%) of Israeli tourists travelled for this purpose, making it the primary reason for visits. 11.8% of Israeli tourists visited for this reason, showing a moderate amount of family or friend-related travel. Together with this, 5.9% of Israeli travellers came for health or medical care purposes, indicating interest in medical tourism.

Israeli tourists are value-conscious but prioritize high quality and safety.

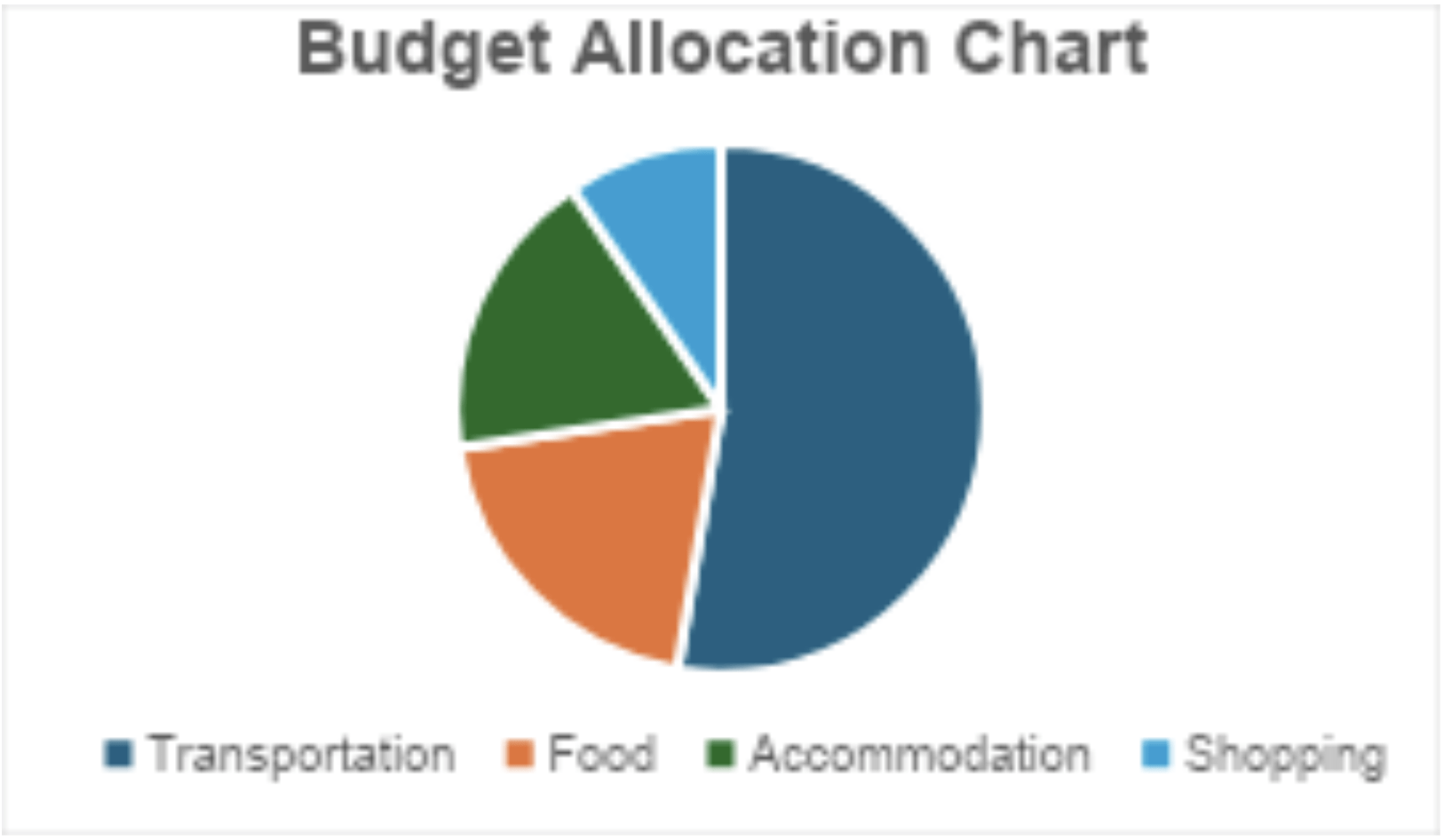

Israeli tourists visiting Azerbaijan recorded total expenditures of 115,670.40AZN in 2025, with an average spending of 2,036.02AZN per tourist.

Budget Allocation: Half of this amount (58,229AZN; 50%) was spent on transportation, indicating substantial internal mobility, while food services (21,767AZN; 19%) and accommodation (19,097AZN; 17%) formed the next largest spending categories. Shopping for goods and gifts accounted for 10,564AZN (9%), whereas expenditures on cultural activities, sports and entertainment, tour packages, and other minor services together represented only a small share of total spending, highlighting a strong focus on essential travel and hospitality services.

A total of 56,812 Israeli tourists visited Azerbaijan during the reporting period, with the majority staying for short to medium durations. The most common length of stay was 1-3 nights, accounting for 25,178 visitors (44%), followed closely by stays of 4-7 nights with 21,863 visitors (38%). This indicates that Israeli tourists largely prefer short city breaks and week-long visits.

Longer stays are less common: 10% stayed for 8-14 nights, while 3% remained for 15-21 nights and 2% for 22-28 nights. Very long stays were rare, with only 1% staying 29-70 nights and a negligible share staying 71-90 nights. Same-day visitors accounted for just 1%, showing that most Israeli visitors include at least one overnight stay. Overall, the data highlights a strong preference among Israeli tourists for brief but structured visits to Azerbaijan.

The most visited regions by Israelis in Azerbaijan are Baku, Gabala, Guba, Gusar, Ismayilli, Shaki and Naftalan.

Israeli tourists show preference for various tourism products such as nature, gastronomy and wine, sightseeing, skiing, hiking, outdoor activities, SPA and wellness. Due to variety of the tourists’ groups subject of interests may significantly vary still falling under the ATB product categories and sub-categories.

Israeli tourists display a strong preference for short and medium city breaks, particularly in urban destinations such as Baku. This is clearly reflected in:

The dominance of 1-3 nights (44%) and 4-7 nights (38%) stays.

High expenditure on transport (50%), indicating frequent movement within cities and nearby attractions.

City sightseeing tours

Old City (Icherisheher), Boulevard, Flame Towers, modern architecture

Cafés, restaurants, nightlife, and promenades

Implication: Baku-centered, compact itineraries with flexible timing are highly attractive.

Israeli tourists show a clear inclination toward independent travel rather than organized package tourism:

Spending on tour packages is negligible (≈0%)

Low use of vehicle leasing

Strong reliance on taxis, ride services, and private transfers (part of transport dominance)

Tailor-made or semi-guided tours

Hop-on/off sightseeing formats

Private day tours with flexible schedules

Implication: Israelis prefer freedom, customization, and spontaneity over rigid group programs.

Food services account for 19% of total spending, making gastronomy one of the top engagement categories.

Local and international restaurants

Azerbaijani cuisine experiences

Wine bars, cafés, casual dining

Implication: Culinary experiences are a strong motivation factor and should be integrated into itineraries rather than treated as add-ons.

With 9% of total spending allocated to goods, gifts, and shopping, Israeli tourists show consistent interest in retail experiences.

Souvenirs, handicrafts, carpets, local products

Modern shopping malls and bazaars

Implication: Shopping opportunities should be included naturally within city tours and free-time blocks.

Accommodation accounts for 17% of spending, suggesting:

Preference for good-quality, centrally located hotels

Balance between comfort and value rather than extreme luxury

3-4 star hotels

Boutique and city hotels close to attractions

Implication: Value-for-money accommodation in prime locations resonates strongly with Israeli travelers.

Very low spending shares on:

Cultural activities (1%)

Sports and entertainment (1%)

This indicates that while cultural landmarks are visited, deep, formal cultural programs are not the main driver of travel decisions.

Implication: Culture should be presented in light, accessible formats (walking tours, combined city experiences), not as stand-alone intensive programs.

Israeli tourists approach Azerbaijan similarly to European short-haul destinations:

Quick decision-making

Short stays

High mobility within limited time

Implication: Azerbaijan is perceived as an easy, affordable, and interesting nearby destination, ideal for short leisure breaks.

Expected outbound trips: 9.5-10.2 million

Growth rate: +5% to +12% compared to 2025

Israel’s outbound tourism market is widely expected to reach new record levels in 2026, driven by:

Continued restoration of international air connectivity at Ben Gurion Airport

Expanded capacity by both Israeli and foreign airlines

High household propensity to travel internationally despite regional risks

Multiple market analyses indicate that 2026 will mark a consolidation-to-expansion phase, with outbound volumes exceeding all previous benchmarks if no prolonged airspace closures occur.

The forecast also reflects structural shifts in outbound behavior:

Short-haul destinations (Mediterranean, Eastern Europe, Caucasus) will continue to dominate in volume

Long-haul travel (USA, East Asia) will recover more slowly but yield higher per-trip spending

New and alternative destinations (including the Caucasus and Central Asia) are expected to further increase market share as Israelis diversify away from traditional routes

These trends support continued outbound expansion even under volatile geopolitical conditions.

Personal relationships and trust are central to business culture in Israel; family, relative, and long-standing friendship ties strongly influence cooperation and decision-making.

It is essential to build direct, friendly, and continuous relationships with partners at all levels, from management to operational staff, as loyalty and personal familiarity are highly valued.

The optimal timing for marketing campaigns is 4-6 weeks before major Jewish holidays, when travel decisions are typically finalized.

Face-to-face meetings, especially in an informal setting, remain the most effective way to establish credibility and advance partnerships.

Participation and attendance rates at physical and online events tend to be relatively low, unless the event delivers clear business value or involves trusted partners.

Small gifts and personal attention during holidays (such as Jewish holidays or company milestones) are well appreciated and contribute positively to long-term relationships.

Key market centers to focus on are Tel Aviv and the Greater Tel Aviv metropolitan area (including Ramat Gan and Herzliya), Jerusalem, and Haifa, which together concentrate the majority of Israel’s travel agencies, tour operators, airlines, and decision-makers.

☐ Define the core value proposition for Israeli travelers (city breaks, lifestyle, gastronomy, shopping, short-haul leisure).

☐ Ensure the destination/product fits short trip patterns (3-7 nights).

☐ Identify target segments: families, young couples, FIT travelers, business travelers, or niche groups (religious, cultural).

☐ Identify key tour operators and travel agencies in Tel Aviv and the Greater Tel Aviv area.

☐ Establish direct personal contact with decision-makers (owners, product managers).

☐ Allocate time for relationship-building, not just transactional negotiations.

☐ Plan for longterm cooperation, as loyalty and trust drive repeat business.

☐ Prioritize Tel Aviv and Greater Tel Aviv (Ramat Gan, Herzliya) for B2B engagement.

☐ Include Jerusalem for group, cultural, and religious tourism segments.

☐ Include Haifa for regional northern outreach.

☐ De-prioritize cities with limited travel-trade concentration (e.g. purely residential or port cities).

☐ Offer flexible, modular products suitable for FIT travelers.

☐ Ensure itineraries emphasize urban experiences, food, shopping, and light sightseeing.

☐ Avoid over-reliance on rigid group packages unless targeting 50+ or religious segments.

☐ Align accommodation offerings with mid-range, centrally located hotels.

Contact person

Director of ATB Israel branch